Banking customers increasingly expect immediate, accurate responses regardless of time or channel. A customer checking a transaction at 2 a.m., disputing a charge on a weekend, or needing quick clarification on a loan EMI often faces delays when relying solely on call centers or branch visits.

These friction points create dissatisfaction and push users toward digital alternatives or competitors.

Conversational AI for banks uses natural language technologies to interpret customer questions in everyday language, whether typed or spoken, and respond with relevant information or actions drawn directly from bank systems.

This capability has gained traction across global and Indian banking because it aligns with the dual pressures of cost control and service quality.

Conversational AI in banking handles high-volume, repetitive inquiries while adhering to strict security and regulatory standards. Industry projections show strong momentum: the global conversational AI market is expected to grow from approximately USD 14–17 billion in 2025 to USD 49–82 billion by the early 2030s, with banking remaining one of the most active sectors due to its large transaction and inquiry volumes.

This article provides a detailed examination of how conversational AI for banks operates in practice, the most common applications, documented outcomes, technical architecture, regulatory requirements (with emphasis on India), implementation realities, and forward-looking considerations.

What is Conversational AI in Financial Services?

Conversational AI refers to software that processes human language input (text or voice), maintains context over multiple exchanges, and generates appropriate replies or triggers backend actions.

Core Building Blocks

- Natural Language Understanding (NLU): Parses input to identify the customer’s goal (intent) and specific details (entities). For example, “What’s my savings balance yesterday?” → intent = balance inquiry, entity = account type (savings), time period (yesterday).

- Dialogue Management: Remembers prior turns in the conversation, asks follow-up questions if information is missing (“Which account, savings or current?”), and decides when to escalate or complete the request.

- Backend Integration: Securely queries core banking systems, CRM databases, payment rails, or fraud engines via APIs.

- Response Generation: Crafts replies that sound natural. Modern deployments frequently incorporate large language models for varied phrasing while constraining output to approved facts and formats.

Earlier banking chat interfaces relied on rigid decision trees with limited branches. Contemporary conversational AI in financial services supports free-form questions, handles interruptions, recovers from misunderstandings, and escalates gracefully when confidence drops or topics become sensitive.

Primary Use Cases of Conversational AI for Banks

Banks prioritize use cases that combine high frequency, clear rules, and measurable value.

Balance and Transaction Inquiries

Customers ask for current balances, recent credits/debits, or mini-statements. The system authenticates the user, pulls real-time data from core systems, and presents formatted summaries.

Payments and Transfers

Users initiate internal transfers, pay utility bills, recharge mobile numbers, or send money via UPI/IMPS. The assistant collects amount, beneficiary details, and executes (or schedules) the transaction after authentication.

Card Operations

Requests to block lost/stolen cards, report fraudulent charges, raise disputes, or adjust spending limits are common. The system guides users through verification and updates card status instantly.

Account Opening and KYC Assistance

Digital onboarding involves collecting personal details, uploading documents, answering eligibility questions, and explaining terms. AI handles initial data gathering and flags incomplete or inconsistent submissions for human review.

Fraud and Security Verification

When fraud rules flag unusual activity, conversational channels enable rapid customer confirmation (“Did you authorize a ₹12,000 purchase at XYZ Store?”). Quick resolution reduces false-positive blocks and improves trust.

Loan, Deposit, and Investment Queries

Customers calculate EMIs, check loan status, inquire about FD/RD interest rates, or seek basic product comparisons. The system provides accurate calculations and links to application processes.

These applications focus on routine interactions that previously dominated contact-center volume, freeing human agents for advisory or exception handling.

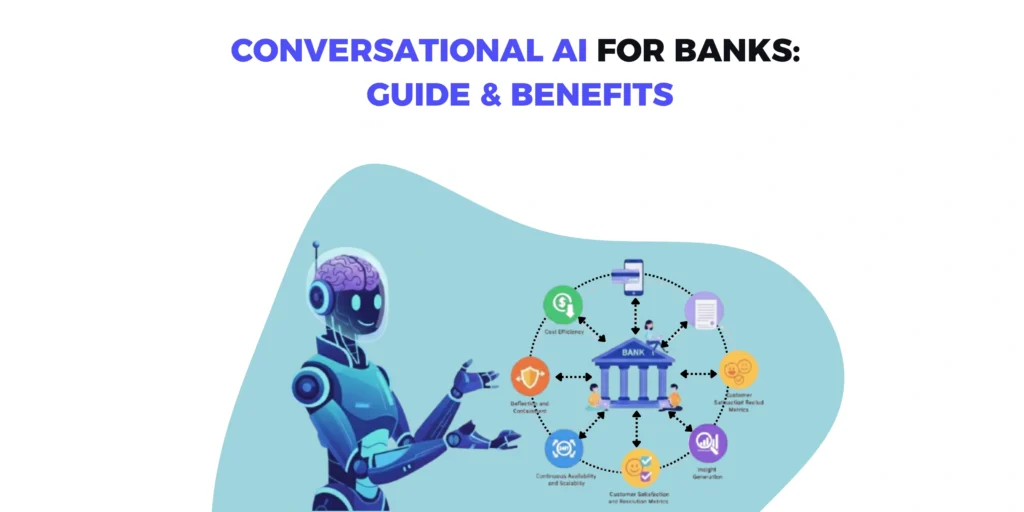

Measured Benefits of Conversational AI in Banking

Deployments produce repeatable improvements across several dimensions.

Cost Efficiency

Automated handling of routine inquiries typically costs 30–60% less per interaction than live-agent support (McKinsey reports on AI-enabled customer service). In high-volume environments, this translates to meaningful operational savings.

Deflection and Containment

Mature implementations deflect 60–80% of level-1 inquiries from human channels. McKinsey analyses of AI in contact centers cite containment rates that significantly reduce assisted interaction volume.

Customer Satisfaction and Resolution Metrics

First-contact resolution often increases because the system provides consistent, accurate answers without misrouting. Response times drop from minutes/hours to seconds, positively influencing CSAT and NPS scores in many reported cases.

Continuous Availability and Scalability

Conversational channels operate 24/7 without staffing increases. During product launches, festive seasons, or unexpected events, the system absorbs spikes automatically.

Insight Generation

Structured conversation logs reveal patterns in customer questions, product pain points, and emerging needs, data that informs service design, marketing, and risk models.

Technical Architecture of Conversational AI for Banks

A typical deployment includes:

- Channel Interfaces, Mobile app chat, WhatsApp Business API, web widget, voice IVR.

- Orchestration Layer, Directs messages based on channel, user profile, and context.

- NLU & Intent Engine, Classifies purpose and extracts parameters.

- Policy & Compliance Engine, Applies bank-specific rules (daily limits, authentication requirements, restricted topics).

- Core System Integration, Real-time API calls to core banking, payment switches, fraud platforms.

- Response & Action Layer, Generates replies and executes permitted actions.

Authentication Mechanisms

Banks enforce step-up authentication for sensitive requests (OTP via SMS/app, device binding, knowledge questions, behavioral biometrics).

Voice vs Text Implementation

Voice requires robust noise cancellation, accent handling, and barge-in support. Text allows richer formatting (tables, links) and easier document upload.

Security, Compliance, and Regulatory Requirements

Banking imposes stringent controls.

Global and Indian Frameworks

- Data Protection, GDPR, DPDP Act (India), CCPA require consent, minimization, and deletion rights.

- Payment Standards, PCI DSS prohibits storage of full card data.

- RBI Guidelines, The RBI’s FREE-AI Committee (2025) outlined principles for responsible AI, emphasizing fairness, transparency, explainability, and customer protection in financial services.

Practical Controls

- Never expose full account numbers or credentials in responses.

- Maintain immutable audit logs of every interaction.

- Use deterministic logic for regulated actions to avoid unpredictable outputs.

- Implement content filters and human oversight for high-risk topics.

- Conduct regular bias audits and model testing.

These safeguards add development and testing overhead but are essential for regulated deployment.

Implementation Challenges and Practical Approaches

Legacy System Connectivity

Many core platforms use older APIs or batch processing. Banks build middleware layers or adopt API-first modernization roadmaps.

Language Diversity

In India, support for Hindi, regional languages, and code-mixing is necessary. Quality training data and continuous tuning are required.

Escalation Experience

Context handoff must be complete, account details, prior turns, intent summary. Poor transitions create frustration.

Success Measurement

Track deflection rate, containment percentage, average resolution time, cost per conversation, CSAT delta (bot vs human), and escalation accuracy.

Conclusion

Conversational AI for banks has progressed from experimental chat windows to production systems that reliably handle substantial portions of customer interactions while respecting regulatory boundaries.

Core lessons include the critical role of secure integration, layered authentication, and ongoing performance monitoring. Practically, banks see the strongest returns when focusing first on high-volume, low-variability inquiries and expanding based on data.

In the coming years, expect deeper integration with real-time payments, proactive alerts, and lightweight advisory functions. Institutions that thoughtfully implement and refine these systems will be better positioned to deliver the instant, accurate, and secure experiences customers now regard as standard.

FAQs

What is conversational AI for banks?

Conversational AI for banks uses natural language processing to interpret customer questions via chat or voice, retrieve data from bank systems, perform permitted actions, and respond accurately while enforcing compliance rules.

How much cost reduction can banks expect from conversational AI?

Well-implemented systems often reduce interaction costs by 30–60% compared with live agents, primarily through deflection of routine inquiries from contact centers (McKinsey service automation analyses).

Is conversational AI secure for sensitive banking tasks?

Yes, when built with multi-factor authentication, data masking, audit logging, and compliance with RBI guidelines, PCI DSS, and data protection laws to prevent unauthorized access or leakage.

What are the highest-impact use cases in banking?

Balance inquiries, transaction lookups, fund transfers, card blocking/disputes, fraud verification, and basic onboarding/KYC support, tasks that represent large portions of daily customer contact volume.

How does conversational AI improve customer satisfaction in banking?

It delivers instant 24/7 responses, consistent answers, context retention across turns, and reduced wait times, frequently leading to higher first-contact resolution and improved CSAT/NPS scores.

What are the main compliance challenges for conversational AI in banking?

Challenges include data privacy (DPDP Act/GDPR), payment security (PCI DSS), explainability, auditability, and adherence to RBI responsible AI principles, requiring strict controls and testing.

Can conversational AI handle complex or emotional banking queries?

It manages routine and moderately complex tasks well but escalates high-risk, advisory, or emotionally charged conversations to human agents to maintain accuracy and empathy.

How long does it take to deploy conversational AI in a bank?

Focused pilots can launch in 4–6 months; full-scale, multi-channel deployments with legacy integration and compliance validation often require 12–18 months.

Which channels are most effective for banking conversational AI?

Mobile banking apps, WhatsApp Business, web chat widgets, and voice assistants perform strongly, aligning with customer preferences for quick, secure, and multi-device access.

What KPIs should banks monitor for conversational AI performance?

Key metrics include inquiry deflection/containment rates, cost per conversation, customer satisfaction after bot vs human, first-contact resolution, escalation quality, and fraud detection accuracy.